What are the implications of the Silicon Valley Bank crash?

Background and Context

What is SVB bank and why is it so important?

The Silicon Valley Bank (SVB) failure marked the largest bank collapse since 2008, highlighting vulnerabilities in the banking system. Located in Silicon Valley, California, SVB primarily served tech startups, leading to a high concentration of deposits from one sector. This risk was exacerbated by the fact that over 90% of deposits at SVB, as well as Signature Bank, were uninsured, leaving many customers exposed. Additionally, the Federal Reserve's monetary policies, including quantitative easing, played a significant role in shaping the challenging financial conditions that contributed to the bank's collapse.

What were the stock market trends during the crash?

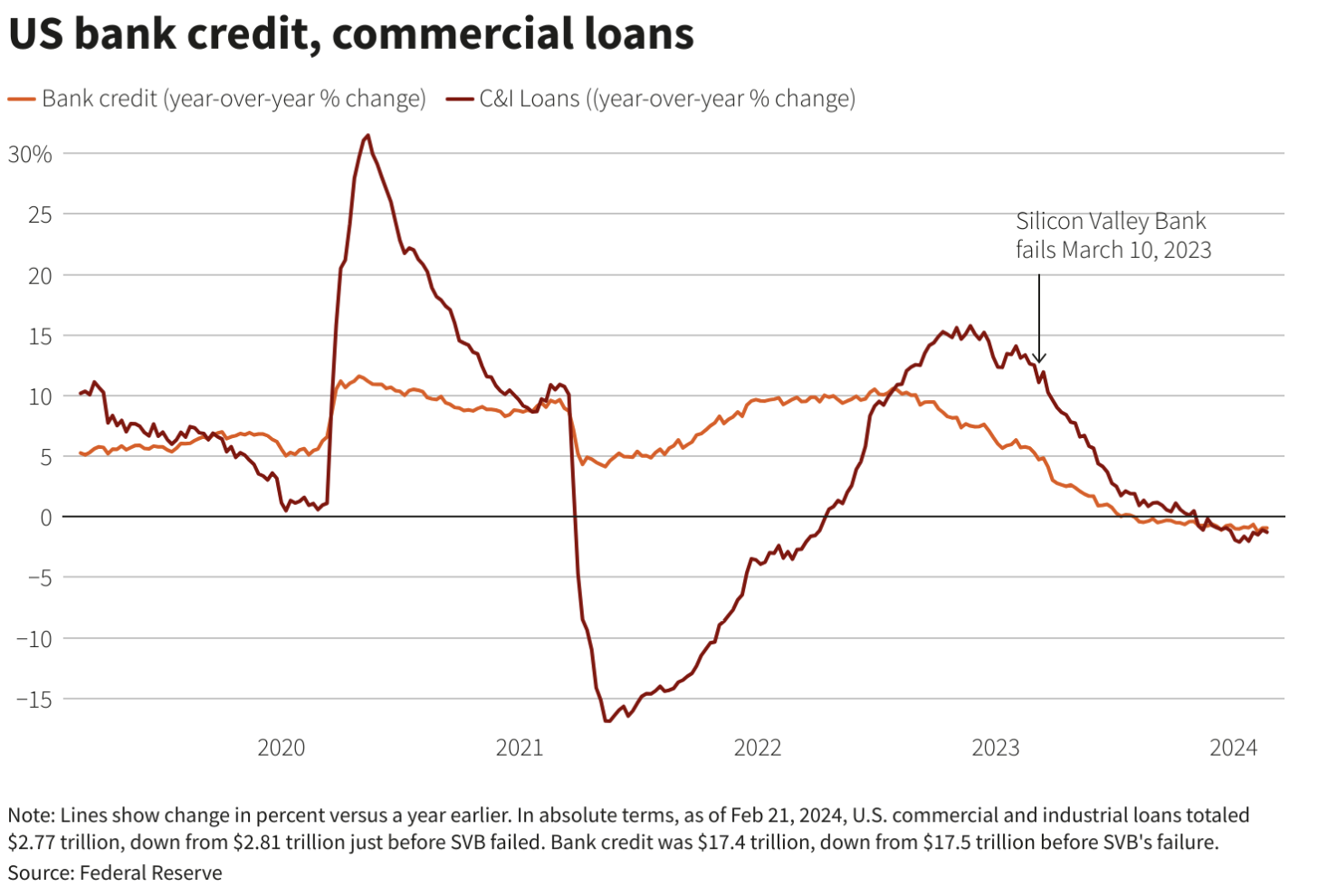

During the Silicon Valley Bank (SVB) crash, the stock market experienced significant turmoil. On Monday morning, March 13, 2023, SVB's shares plummeted by 60%, reaching a new 52-week low. This sharp decline followed the bank's sale of approximately $21 billion in securities, resulting in an after-tax loss of $1.8 billion for the first quarter of 2023. The broader U.S. trading environment was marked by heightened volatility, with concerns about financial stability spreading across markets, particularly in the banking and tech sectors. The graph on the right indicates a rapidly declining number of commercial loan totals shortly after the crash.

What is the future of the US Stock Market?

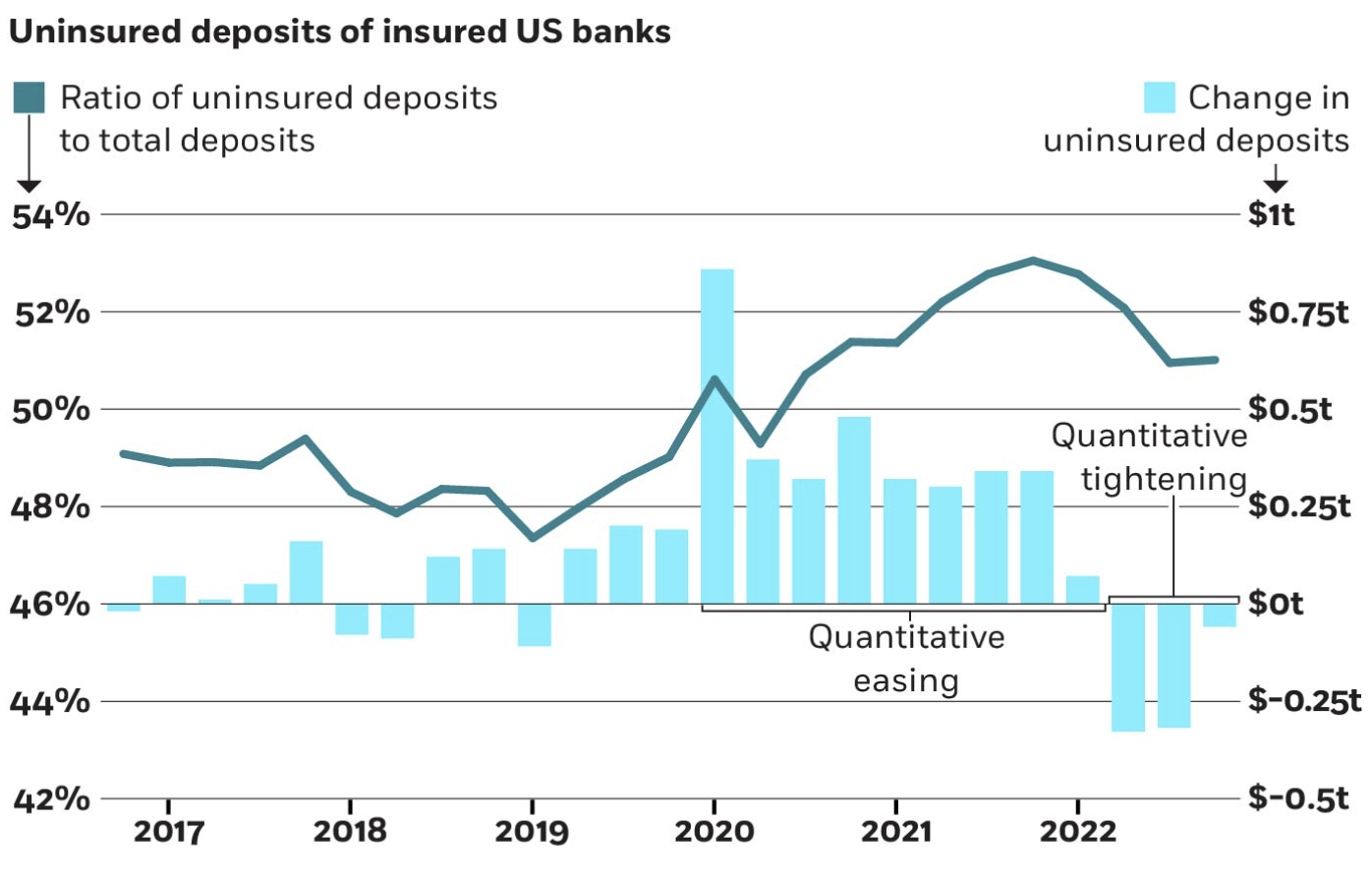

The collapse of Silicon Valley Bank (SVB) not only tarnished Silicon Valley's reputation as a hub of financial savvy but also had a widespread negative impact on global markets. Studies show substantial declines across major indices, including the top nine global equity indices, 53 global stock indices, and 43 financial sector indices, highlighting the ripple effects of the SVB crash on both domestic and international markets. The graph on the left depicts the US uninsured loan deposits growing as we approach the SVB bank crash, as discussed above because most of SVB loans were uninsured.

Information Availability

1. Impact on Banking Sector (Both national and international)

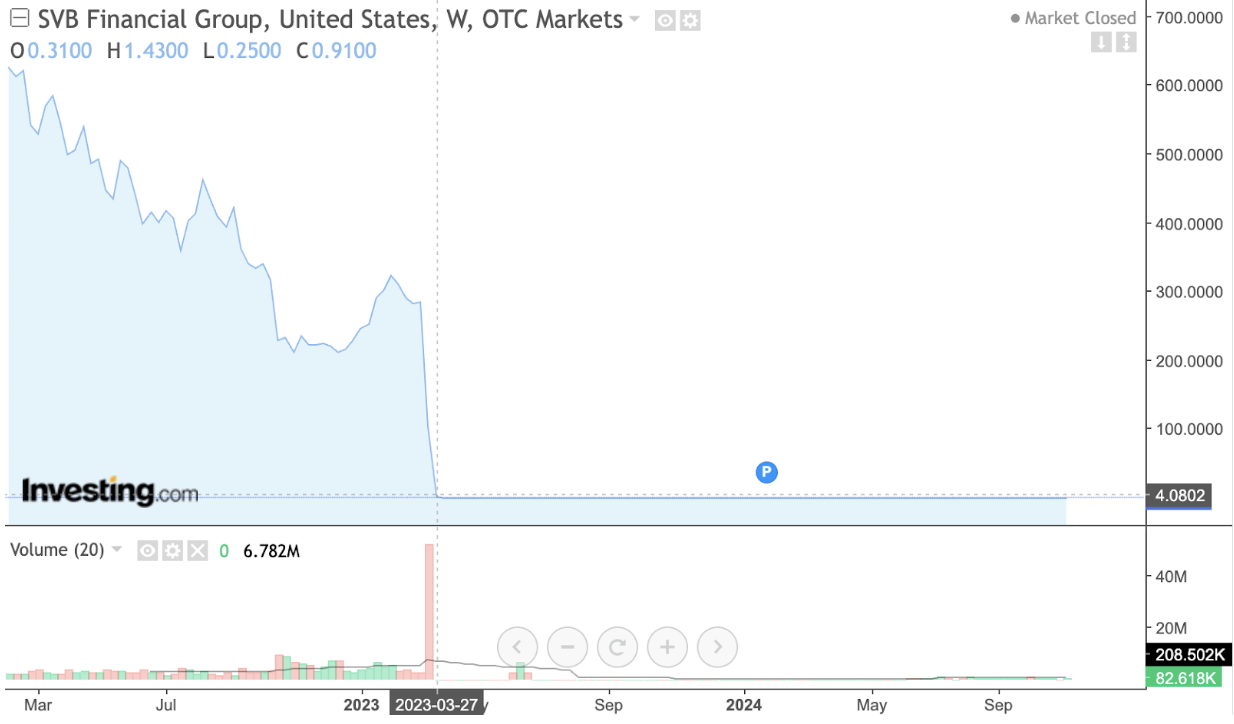

Political contagion caused many other regional banks to experience decrease in investors. Regional lenders such as the First Republic Bank saw its shares fall as much as 52% during early trading, and it continued to drop afterward. The graph below indicates a steep decline in SVB stock after March of 2023 indicating how much trust was lost in a singular month.

2. Legal Repurcussions

FDIC filed a lawsuit against 17 former executives and directors of SVB claiming gross negligence and breaches of fiduciary duty. They are trying to recover billions of dollars lost due to the collapse, which the FED is being accused of contributing to.

3. Political Discourse

The political debate during the Silicon Valley Bank (SVB) crisis centered on how President Biden handled the fallout. Republicans, like presidential candidate Nikki Haley, criticized the administration's response, arguing it was effectively a bailout and unfairly placed the burden of SVB’s mismanagement on depositors at healthy banks. They expressed concerns that the Deposit Insurance Fund could deplete, leaving all bank customers vulnerable. Meanwhile, Democrats defended the measures as necessary to stabilize the financial system and protect depositors.

4. Ongoing Concerns

The collapse of Silicon Valley Bank (SVB) raised critical questions about changing interest rates and the future of Federal Reserve policies. It also fueled debates about market performance and whether the public should continue entrusting their money to banks. The rise in uninsured deposits underscored the urgent need for improved public financial literacy, as many depositors lacked awareness of the risks. Additionally, the steep drop in SVB deposits highlighted vulnerabilities in banking practices and the importance of diversifying financial strategies.

Insights

1. Since 94% of the deposits of Silicon Valley Bank and Signature Bank were uninsured, compared to the national average of around 50%, there is a deeper motivation for the public to be financially literate and ensure they are investing their money with full awareness of the risk.

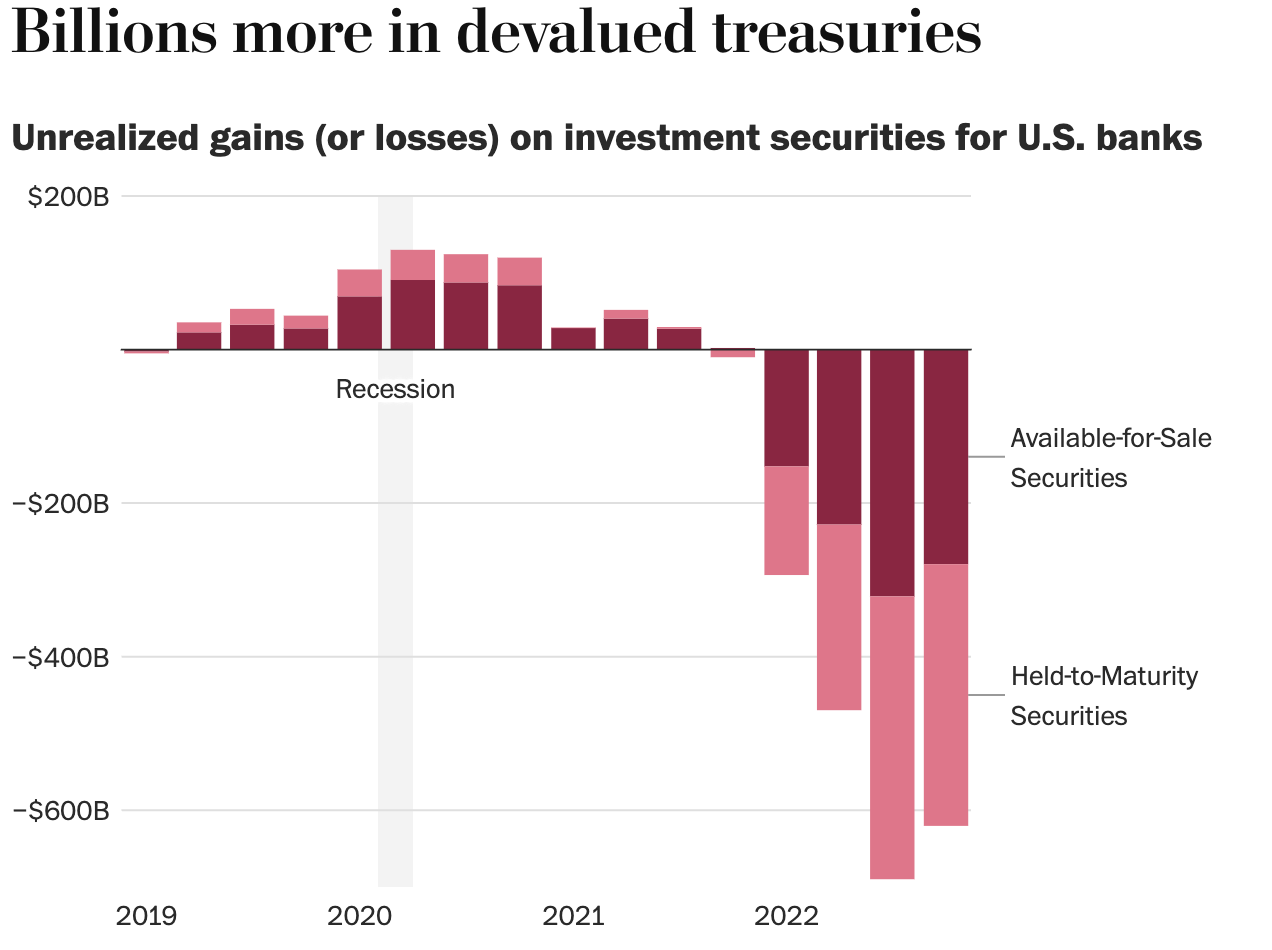

2. The financial sector needs to reconsider the unrealized potential of depreciating bonds. U.S. banks are sitting on a staggering $620 billion in unrealized losses, according to the FDIC on the graph to the left. The problem only continues to deepen as short term solutions to this problem continue to arise.

3. Silicon Valley Bank (SVB) collapsed due to its heavy investment in fixed-rate securities during the pandemic, which made up 60% of its assets by the end of 2022. As the FED raised interest rates, the value of bonds dropped, creating a $15 billion shortfall in its $91 billion portfolio, which can be seen on the graph to the right. Then, when depositors withdrew $42 billion in a single day, SVB was forced to sell its securities at massive losses, leading to its collapse. The public can realize the inverse relationship between interest rates and bond value, to ensure they are aware of when their money is at risk.

Closing Thoughts

The public should understand that while the collapse of SVB and Silvergate Bank has raised concerns of financial instability and drawn comparisons to the Great Recession, these failures are primarily linked to their focus on high-risk sectors like cryptocurrency, startups, and venture capital, which are more sensitive to interest rate changes. Analysts emphasize that most banks today serve a broader range of customers, which helps protect them from similar risks. This gives hope that all moves for recovery are not lost, and historical data only depicts the numbers, and there is more to the situation than that.

Sources